An urgent message from Jim Rickards, one of America’s top financial forecasters…

An urgent message from Jim Rickards, one of America’s top financial forecasters…

It should’ve been a day like any other…

You’re at the gas station filling up your ride.

You head into the store to pay.

“$77 please,” says the cashier.

You pull out $80 in cash and slap it on the counter.

“Sorry, sir. No cash. We only take cards from now on.”

With a grumble, you pull out our debit card and swipe it.

“Thank you, sir. Just so you know, a note on your credit says you’re almost up to your $80 limit in gas for the week. You’re getting close to your government allotted carbon emissions for the month…”

Walking out of the store, you wonder what the heck he was talking about…

You drive to your next errand. Along the way, you notice a long line in front of an ATM machine.

You stop to check it out. People are walking away from the ATM in frustration…

You stop and ask what’s going on…

“The machines stopped giving out cash,” you are told.

Now you feel that little twinge of fear in your gut. You know that feeling?

You knew things were getting bad. But surely things are not that bad…

You check your phone: No wars. No terrorist attacks. No hurricanes or earthquakes.

Still, something is up. It’s getting weird out there, fast…

You head inside the grocery store to pick up dinner.

As you head into the store, you notice long lines at the check-out counters.

Anger is in the air. The smell of panic…

A woman grabs your arm:

“They say ‘card-only’ but my card isn’t working… NOBODY is taking cash… and they’re running out of food…”

You turn around and head out…

In the parking lot, you send a text to your friend.

He’s one of those political “gun nut”-types, so maybe he’s got some insight to share…

“Things are getting scary. I went to the sporting goods store to grab some supplies and ammo. They’re telling me that based on my google search history and the websites I’ve visited… I can’t buy anything, even with cash. I checked my account and I have plenty of money. But they won’t let me spend it! They’re saying I’m flagged as a threat?!?!”

You text a few more of your friends…

One says his business can no longer take payments from customers. He wonders if it’s because he donated to that “freedom for America” protest…

Heart sinking, you remember all those donations you made recently…

Another friend urgently texts you… none of her cards work, either. Her online payments are not going through, and her rent is due.

You feel yourself start to sweat. Tomorrow is the end of the month. You have a bunch of bills due…

Another friend says he’s hearing about violence in the streets… people smashing and grabbing whatever they can… banks locking their doors on customers…

Your mind races. Some sort of system-wide banking crash, you suspect.

You rush home…

It’s OK, you tell yourself. You’re prepared. You have a couple thousand in cash under the mattress. Plus, you’ve got your savings account and 401k nest egg…

You check your banking app on your phone. You are greeted with the following message:

“Dear Customer, please be advised certain purchases may be limited or not be permitted according to Federal law.

All our ATMs and branches are currently shut down until further notice.

If you wish to speak with one of our representatives, please be aware we are experiencing higher than normal call volume and wait times will be longer than expected. Thank you and have a nice day…”

You turn on the TV to get the news.

Images flash on your screen of long lines at supermarkets and gas stations… stock market indexes in the red… riot police and National Guardsmen in the streets…

The news anchor is nodding his head solemnly:

“Today, the White House directed banks and other financial institutions to stop doing business with thousands of Americans, freezing their personal bank accounts…

Palms sweating, you switch to the financial channel:

“Chaos on Wall Street today, after Congress authorized another round of stimulus payments directly into the spending accounts of every American, a move critics say will only increase inflationary pressures as prices spin out of control…”

You flip again:

“Violent protests continue to spread from the cities into the suburbs, in the wake of record unemployment and reports of enforced rationing of electricity and natural gas…”

In the distance you hear sirens…

Breaking glass…

Are those gunshots?

It’s been a hell of a day.

And it’s going to be a long night…

Make no mistake, C-Day will change your financial life forever…

Hi, my name is Jim Rickards…

And the scenario I just described hasn’t happened, yet…

Nonetheless, I’m expecting it will come to pass — and sooner than you might believe is possible.

This might all seem far-fetched.

But I’ve made predictions on this scale before. And I’ve been right…

In 2016, I predicted Brexit would pass. I also predicted some investments which would skyrocket as a direct result. It happened… and some of my readers made 200% on their money. That’s TRIPLE their money in return.

I predicted President Trump would beat Hillary Clinton and win that election.

In 2019, I predicted exactly what played out in the recent Covid crisis…

A full 8 months before the coronavirus pandemic hit our shores, I predicted a “pandemic” leading to a stock market crash, which would also “flood the streets with violence.”

The market tanked thanks to Covid, and we saw cities burn thanks to Antifa and other violent rioters.

I’m a New York Times bestselling author of other books you may have heard of, including Currency Wars and the Death of Money.

I’ve a contributor to publications like The Financial Times, Evening Standard, New York Times, and Washington Post

I’ve also been an advisor to the Office of the Director of National Intelligence — that oversees the NSA, the CIA, and 14 other U.S. intelligence agencies.

In short: I’ve been sounding the alarm on this issue for over 10 years now,

at the highest levels.

And despite my warnings, the danger of “C-Day” continues unabated.

Take a look at this image…

This image reveals something shocking… even sinister…

It’s the first step to something I call “C-Day”… the biggest change in our money supply you’ve ever seen…

It will be more disruptive than the inflation we saw in the 1970s…

Bigger than banking shutdowns of the Great Depression…

More historical than the hyperinflation in the 1930s which led to Nazi Germany and World War II.

If this sounds scary, please understand… it’s OK to be worried!

I’m worried too. That’s why I created this special presentation… to share my research on this situation, along with the steps I’m personally taking to prepare for this event.

In fact, I’m paying money out of my own pocket to get this into your hands.

So please. Please don’t close this window. If you leave this page, I can’t guarantee it will still be up…

And you do NOT want to miss out on getting this critical information.

Because when “C-Day” hits, we will be witness to the biggest disruption we’ve ever seen to our banking and financial system.

As a direct result, American’s #1 safest asset will literally disappear… overnight!

But it could get even worse:

- You could be limited where you spend your money from your account. Certain purchases simply won’t work at point-of-sale. Money will be “programmed” by government agencies or corporations to only work on purchases they pre-approve…

- You could be forced to spend certain amounts of money within certain times, and your bank accounts could be penalized for holding “too much” money with severe negative interest rates…

- Payments from your investments… you employer… your customers… or even the Social Security office could be limited or even shut off based on whatever is financial policy for the U.S. government. Your account can simply be “turned off” from accepting payments from certain individuals or companies.

- Say the “wrong” thing on social media, and you could be locked out of your bank accounts, unable to spend or transfer money…

- Purchases of gasoline… energy…meat… ammunition… even medical care and medications could be limited, or even suspended, based on political whims. (Forget changing the 2nd All purchase of firearms could be instantly stopped without a single law being passed!)

- Websites and other media accused of “misinformation” could be shut down… without any need for direct censorship. The government or banks will simply turn off their bank accounts…

If this seems like a stretch, consider carefully what I have to say next:

There is a massive change coming to our money — a chance that’s more radical than anything we’ve seen in 600 years…

Indeed, this change is a dagger aimed at our financial throats.

And it’s coming faster than you might believe.

Indeed, according to my latest research, “C-Day” could arrive as soon as September 19th…

In the next few minutes, I will break down why I know these events are happening. You can make your own judgments on my forecast.

I’m NOT going to bore you with economic trivia, or give you an academic lecture.

Instead, I’m going to walk you through my C-Day thesis in the simplest terms possible.

This way, you can be ready.

I’m also going to give you the specific steps you can take today to protect yourself, your family and your wealth.

There are easy ways to prepare, and even profit from C-Day…

You don’t need any investing experience to take advantage of these opportunities. Just the knowledge I am sharing with you today…

But I’m jumping ahead. Let’s get back to C-Day and what it means for you…

The Death of America’s #1 Safest Investment

What we are about to see is the end of what’s been considered “America’s #1 Safest Asset” for over a century…

Specifically, I’m talking about the death of the cash version of the U.S. dollar.

In short, I’m predicting cash, including paper money and coinage, will soon become worthless.

The U.S. government and Federal Reserve will simply require all transactions become cashless.

I don’t know what the history books will call the fateful day when this happens…

But I’m calling it “C-Day”… the day America goes cashless.

Before we go into the deeper implications of this, consider this:

The elimination of physical cash alone will have profound consequences…

If you think about it, cash has always been one of our safest and secure assets:

- As a store of value, cold hard cash was the asset of last resort. To protect against a bank failure, you could always stuff cash under your mattress. Or you could bury it in your backyard… or hide it in your freezer…

- Cash transactions between individuals were 100% private and difficult to trace. It took enormous resources to mark and track individual bills…

- Cash was relatively easy to transport. You could stick it in your wallet — or in larger amounts, stuff it inside a briefcase. When I’ve traveled overseas, I’ve hid cash in my shoe…

- Cash was accepted by everyone, anywhere — regardless of whatever insane edicts were coming out of Washington or large corporations…

- Cash, especially U.S. dollars, were a universal means of exchange. Even if inflated, you could use U.S. dollars in cash in every country in the world, including North Korea…

- If you held enough physical cash, you had options and you couldn’t be entirely “canceled” by the system…

Starting on C-Day, poof! All these benefits of paper money could cease to exist.

Does the end of cash seem preposterous?

Just think about what we’ve seen through the Covid… the lockdowns… the increasing control over our daily lives by the Deep State and Big Tech…

And the scary part is…

The “cashless society” is already here…

In many ways, we already live in a cashless society…

According to a study by the Diary of Consumer Payment Choice, cash payments represented 19% of all transactions in the US in 2020.

This was 7 percentage points down from 2019. And I’m sure it’s dropped even more during the past two years…

This means if you are an average American, you use non-cash (your debit card, credit card or phone) around 81% of the time.

You probably know people who NEVER carry cash.

I know some 20-year-old kids who use their cards and phones for every single transaction. They are already 100% cashless.

And increasingly, as a consumer, you don’t even get a choice to use cash or not.

You’ve likely already seen it in your daily life…

Think about it: How many signs have you seen at restaurants… stores… gas stations… all saying:

“No cash, cards only.”

If someone manages a store, they can order a sign like this from Amazon…

In Sweden, many churches and even the homeless won’t accept cash. They take digital cash only…

No more cash in the offering plate on Sundays.

And your local panhandler wants his handout using your phone…

Covid has skyrocketed this trend…

Millions of people now order their food on their phones. They order groceries from apps. They order countless other items from Amazon…

Remember this: Every digital transition is a cashless transaction.

Of course, as of right now, cash is still legal tender in the U.S.

And while most stores haven’t banned cash… yet…

Most soon will…

According to the New York Times,

“From a cup of coffee to a car ride, mobile devices or plastic cards are becoming the preferred, and sometimes exclusive, methods of payment in many parts of the world…”

Walmart is converting some of its self checkout registers to card only. No cash accepted in those lanes, so don’t leave home without your cards or phone…

Even small businesses are falling in line. According to a recent survey commissioned by Square, the San Francisco-based mobile payment giant:

“Small business owners believe the nation will completely ditch paper money… and that the pandemic will accelerate the switchover.”

And a study by Pew Research concludes,

“Consumers increasingly are using credit or debit cards to pay even for low-cost purchases, such as a cup of coffee, surveys show, and apps such as Venmo and Apple Pay are becoming more popular. Credit card companies — which charge retailers fees every time a customer uses a card — have encouraged businesses to stop taking cash…”

It’s happening overseas, too.

According to a story in UK’s Guardian:

“Within days of shops starting to close, UK cash usage halved. Signs reading “contactless payment only” became common at tills and petrol stations. “What covid did was push anyone who could go digital to go digital,” says Natalie Ceeney of the Access to Cash Review, an independent body assessing the future of Britain’s cash needs. The UK has been moving towards a cashless economy for some time, with ATM usage declining at about 6% to 10% a year. But Covid-19 supercharged this transition. “During lockdown, cash withdrawals from ATMs were down about 60%,” she says. “That’s a huge drop.”

Bottom line: Cash as money is already fading away.

For most of us, cash is barely in our pockets or wallets, if at all…

Retailers are increasingly refusing paper money…

The dominos are already tipping over… America is going cashless… it can’t be stopped now.

All it takes now is an edict from the Federal Reserve, or an executive order from President Biden to make it official.

A headline by the New York Times sums up the intentions of the global elite: “The end of cash is on the horizon…”

And make no mistake: A cashless society will change our lives… in ways you’ve probably never considered…

Good Luck Using Electronic “Money” When The Electricity Goes Out…

What does the death of cash mean?

- It means no more cash you can hide if there’s an emergency (national or personal) and you need to get out of town, fast…

- It means no more purchases without the risk of bank transfer fraud…

- It means without access to electricity and the Internet, your money won’t exist (good luck spending digital money if there’s a power outage due to a hurricane, natural disaster, war, or terrorist attack)…

- It means no more cash to spend at garage sales or farmers markets…

- It means no more cash or coin donations to any homeless people you pass on the street…

- It means no more cash slipped into the hands of a grandchild by a grandparent…

- It means no more handing cash to the 14-year-old kid who mows your lawn or shovels your driveway…

- It means no more coins to toss in a wishing well or fountain…

- It means no more cash inside birthday cards…

- It means no more piggy banks or tooth fairy visits for your child or grandchild…

- It means if you travel overseas and your cards get shut off, you could be stuck having NOTHING to pay with…

- It means no having no access to money if you lose your credit or debit cards (or if they are stolen)…

But this is only the start.

Because what will take the place of cash is something even worse…

Cashless is only the start…

Money as cash has existed for 4,000 years going back to ancient Babylon.

What’s the future of money after America goes cashless?

In short, a brand new monetary system.

One we’ve never seen before, in the history of civilization…

Under this new monetary regime, banks would have full control over every digital cent in “your” accounts.

Every transaction would be recorded.

Privacy as we know it would be over…

How?

In short, without cash existing in the physical world, the U.S. dollar will evolve into something called a “Central Bank Digital Currency” or CBDC…

How do I know this is coming?

This is NOT a conspiracy theory.

In fact, President Biden is touting it loudly and for all to hear…

According to a story in NBC News,

“The Biden administration is throwing its support behind further study and development of what would be known as a U.S. Central Bank Digital Currency…”

According to Biden,

“My Administration places the highest urgency on research and development efforts into the potential design and deployment options of a United States CBDC…”

Straight from the horse’s mouth, as the saying goes…

Bitcoin’s Evil Cousin

What is a central bank digit currency, or CBDC?

Let me sum up in as simplistic terms as possible:

CBDCs are the central bank currencies you already know (dollars, yuan, euros, yen, sterling) but transformed into fully digital versions.

They are 100% digital currencies, recorded on a ledger (maintained by a central bank or Finance Ministry), and the transactions are encrypted…

You might think, this kinda sounds like Bitcoin, right?

Well, despite what you might have heard, CBDCs are not cryptocurrencies…

On the surface, they resemble Bitcoin’s evil cousin…

But really, CBDCs have nothing to do with private currencies like Bitcoin.

For one, these are currencies issued by central banks…

They are not created by individuals through crypto mining.

They don’t use the blockchain.

And they definitely do not embrace the decentralized issuance model hailed by the crypto crowd.

In short, CBDCs are mutated freaks of central bank currencies — with all the worst qualities of central bank currencies magnified.

Some people warn that this digital currency could turn into “programmable money.”

Because with it, the government would be able to program what you can spend your money on… how much of it you can spend… and, most importantly, what you can’t buy with your own, hard-earned money.

And as you will soon see, these currencies are extremely dangerous.

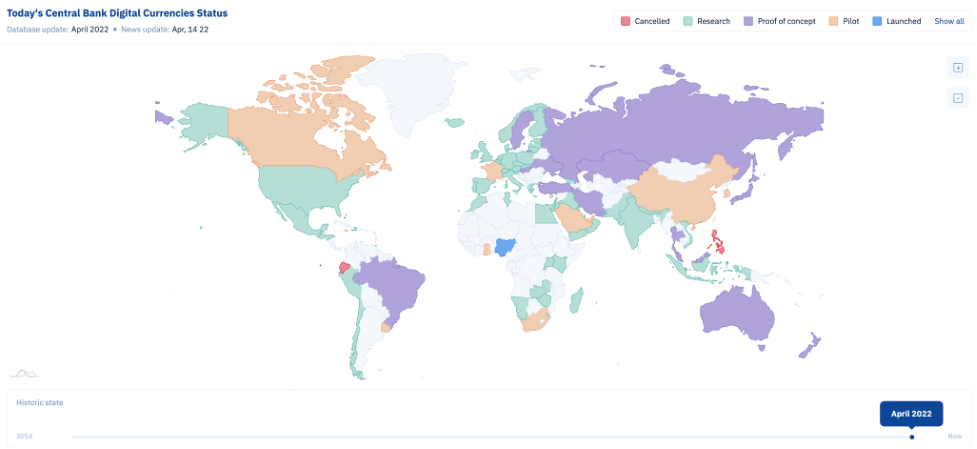

At this very moment, CBDCs are currently being introduced by almost all the major central banks around the world — including research that’s now underway right here in the United States, thanks to Biden’s recent directive

As many as nine countries have already fully launched a central bank digital currency… including The Bahamas, Nigeria, and seven countries in the Caribbean.

And more are on the way, including:

- India. In February 2022, India’s finance minister announced that the Reserve Bank of India is introducing a digital rupee as soon as this year. If it sticks to its plans, India will be one of the largest economies to issue a CBDC…

- Russia. The Bank of Russia first announced plans to launch a digital ruble in October 2017. Facing global sanctions from the war, I’m anticipating Russia’s plans will only accelerate…

- China. According to CNBC, “The People’s Bank of China, the country’s central bank, has been working on the digital form of its sovereign currency since 2014… it’s designed to replace the cash and coins already in circulation.”

Is the USA next?

You better believe it…

That’s why I’m writing you this letter.

To warn you that once cash is outlawed, the U.S. dollar could transition overnight into a full-blown CBDC…

The End Game of the Central Bankers

Why does all this concern me?

And why should it concern YOU?

One big reason:

CBDCs will be highly centralized and tightly controlled by central banks…

I know this to be certain because I’ve been studying and tracking the central banks for over my entire 40 year career.

I’ve written six books on the dangers of central banking, starting with The Death of Money: The Coming Collapse of the International Monetary System in 2014…

And most recently, in The New Great Depression: Winners and Losers in a Post-Pandemic World.

I’ve worked at the highest levels of the finance and intelligence communities…

I’ve been inside the secure meeting rooms called vaults inside of the Pentagon and the CIA.

I’ve been inside the West Wing of the White House.

I’ve been inside the U.S. Treasury and talked to Tim Geithner.

I’ve been inside the boardroom at the Federal Reserve and I’ve personally had conversations with Ben Bernanke.

All of my work has pointed to the scenario I’ve laid out for you today…

I know how central bankers think.

I know how they operate.

I know their ultimate agenda.

And once you understand it, it will chill you to your bones.

Bottom-line, a government-issued digital currency will give the government the ultimate control of the economy…

It will give them complete access to every citizen’s pocketbook.

And nothing will be off the table, especially as the economy spirals into recession and America continues to descend into chaos…

What do I mean?

For starters, one thing I believe they will certainly try to do is “stimulate” the economy.

And they will attempt this by depositing digital funds directly to every American’s account.

It could happen instantly, at a touch of a button. You might wake up and find CBDC dollars deposited in your account without your authorization.

This might seem great. Free money for all, right?

Of course, you and I have worked hard for our money. We know the real meaning of a buck…

Handing out money like this is a moral hazard. It’s the welfare state on steroids.

And worse, “free money” like this will lead to a hyper-inflationary disaster…

More on this in a moment.

But let’s look at one more major implication…

Negative Interest Rates

This new monetary regime could also introduce what economists refer to as “negative interest rates.”

Instead of being limited by a zero-bound threshold on interest rates, the government could impose negative rates on digital accounts.

It’s already happening in China…

As reported by CNN on Nov. 19, 2020,

“China borrows at negative interest rates for the first time… The Chinese sale… included 5-year debt priced with a yield of minus 0.152%.”

This means the Chinese bondholders are losing money simply by holding the bonds.

Why is China doing this? Because they don’t want citizens “hoarding” cash money out of the central bank’s control.

Remember, China’s central bank is also on the verge of launching its CBDC. It’s all part of the plan…

To quote the Wall Street Journal,

“The main monetary power of the digital dollar comes from the abolition of bank notes. If people can’t hoard physical money, it becomes much easier to cut interest rates far below zero; otherwise the zero rate on bank notes stuffed under the mattress looks attractive. And if interest rates can go far below zero, monetary policy is suddenly much more powerful and better suited to tackle deflation…”

Now, I can see why the ability to steal money with negative interest rates is an attractive idea to a central banker…

But what happens to your average citizen, like you and me?

It means your bank accounts could be penalized with negative interest rates for holding “too much” money…

Instead of earning interest on your hard-earned savings, bonds, or Treasury Notes, you will LOSE money every day you hold it…

And this loss is in the form of money taken directly from your account. It doesn’t even factor the loss of purchasing power due to inflation…

In short: They will MAKE you spend instead of saving, using negative rates.

As explained by David Yermack, a finance professor at New York University,

“If the (dollar) is electronic, the government can just erase 2 percent of your money every year…”

Personally, I believe a 2% theft of your money per year is a conservative estimate.

They will likely steal much more…

And not just your money. But our very way of life…

Social Credit

C-Day means the U.S. government and other governments will have increasing control over your money, and thus your life.

Why? Because the government and the banks are increasingly the same entities…

Remember what happened to the truckers in Canada protesting the Covid mandates?

The truckers saw their personal bank accounts frozen, or even seized…

The Canadian government froze up to 206 bank accounts linked to convoy organizers, together worth $7.8 million under emergency measures enacted by Prime Minister Justin Trudeau.

According to a Fox News report,

“Derek Brouwer, a Canadian truck driver who attended the ‘Freedom Convoy’ in Ottawa, said his bank accounts have been frozen… Brouwer said his personal bank account, his trucking account and a third unrelated business account were all frozen over the weekend…”

And let’s not forget it became impossible for truckers to receive payments or donations because GoFundMe blocked $10 million donations destined for “Freedom Convoy” in Canada…

But this hasn’t been isolated to Canada…

Recently, in Russia, governments, banks and payment processors have cut off services to common citizens.

The Associated Press reports Mastercard and Visa are suspending their operations in Russia:

“Mastercard said cards issued by Russian banks will no longer be supported by its network and any card issued outside the country will not work at Russian stores or ATMs.”

But there’s more. According to the Verge,

“Customers at a number of banks in Russia can no longer use their bank cards with Google Pay and Apple Pay due to newly-imposed financial sanctions on the country…”

Irish journalist Jason Corcoran reported,

“Apple Pay and Google Pay no longer work on Moscow’s metro system, leading to long queues as people fumble about for cash…”

Just imagine the chaos if cash is outlawed, and cards are cut off like this!

And there are bigger plans in the works for even more control over the accounts and purchases of average citizens…

According to the Telegraph,

“The Bank of England has called on ministers to decide whether a central bank digital currency should be ‘programmable’, ultimately giving the issuer control over how it is spent by the recipient…”

Tom Mutton, a director at the Bank of England, said programming could become a key feature of any future central bank digital currency:

“You could introduce programmability - what happens if one of the participants in a transaction puts a restriction on [future use of the money]? There could be some socially beneficial outcomes from that, preventing activity which is seen to be socially harmful in some way. But at the same time it could be a restriction on people’s freedoms…”

Getting the picture yet?

This new digital money could easily be “programmed” to create limits in purchases of gasoline or meant (because of “global warming”)…

Why bother trying to fight the courts over the Second Amendment?

Governments could simply “program” your cards to not purchase guns or ammo.

Medical care could easily be rationed by politicians or corporations…

Imagine you show up to the clinic and find out your card is rejected because your account was “programmed” to spend only a certain amount of money on medical care or medications…

There is a word for all this. It’s called “social credit.”

Such a system already exists in places like China.

According to The Federalist:

“The Chinese Communist Party tracks its people’s economic decisions and even things like being a good or bad driver to reward or punish behavior. Punishment might include anything from slower internet speeds to being barred from flying or staying in certain hotels. There have also been reports of people being denied higher education and having their pets confiscated…”

Imagine the power to enforce “social credit” on Americans once the dollar is 100% digital and you can’t pay for anything with paper money?

But there is something even more destructive which could be unleashed…

Hyper-Inflation

If the Federal Reserve can print money with the touch of a button and drop digital dollars directly into the accounts of millions of Americans, what will happen with inflation?

A fully digital dollar CBDC will mean the ultimate money printer…

This could easily cause hyper-inflation.

According to a paper published by Jeffrey Gundlach, chief executive of California-based investment management firm DoubleLine Capital:

“With CBDCs, the central banks would possess the necessary plumbing to directly deliver a digital currency to individuals’ bank accounts, ready to be spent via debit cards. Such a mechanism could open veritable floodgates of liquidity into the consumer economy and accelerate the rate of inflation.”

According to a report by Reuters,

“A central bank digital currency, or CBDC, could bring even more monetary disruption than the early days of paper money. With a digital currency, no printing press or commercial banker stands to impede the flow of newly created money into the economy. After the bankruptcy of Lehman Brothers, central banks conjured up plenty of dollars, euros and pounds but quantitative easing didn’t spark much inflation since banks deposited most of the money straight back at the central banks. A newly issued digital currency, on the other hand, would go directly into people’s pockets…”

Ask yourself, do you trust our central bankers to NOT open the floodgates to spending money if they can easily do so?

I could rattle off dozens of examples of hyperinflation from the 20th century alone… Venezuela, Argentina, Brazil…

Consider what happened in Hungary in 1946…

Few people know that the worst hyperinflation ever recorded was not the German hyperinflation of 1923 or the hyperinflation in Zimbabwe 2008…

It was in Hungary. The post-World War II hyperinflation of Hungary held the record for the most extreme monthly inflation rate ever — 41.9 quadrillion percent, with prices doubling every 15.3 hours.

Which meant a loaf of bread more than tripled in the course of a day.

Of course, the hyperinflation in Hungary also leveled its economy…

According to Business Insider,

“Real wages fell by over 80% as a result of the inflation, and though the workers had jobs, they were pushed into poverty by the hyperinflation…”

Will the U.S. be facing a similar scenario if cash is outlawed, a CBDC digital dollar is launched and we face C-Day?

It’s certainly a possibility…

But even if we only face a smaller-scale disaster, you need to be ready…

History Repeating

Don’t believe me that the U.S. government would go ahead with something like this?

The fact is, they’ve done it before.

You see, back in the 1930s, our dollars were still based on gold.

But the U.S. government and the Federal Reserve didn’t want citizens to use money based on gold.

Do you know what they did?

They outlawed it.

On April 5, 1933, President Franklin D. Roosevelt signed Executive Order 6102.

This executive order outlawed gold as money, “forbidding the hoarding of gold coin, gold bullion, and gold certificates within the continental United States.”

Any violation of the order was punishable by fine up to $10,000 (equivalent to $209,000 today), up to ten years in prison, or both.

Regular Americans faced literal persecution for trying to use gold as money…

- A New York attorney named Frederick Barber Campbell had a deposit at Chase National Bank of over 5,000 troy ounces of gold. Campbell attempted to withdraw his gold, but the bank refused to give him anything other than paper dollars. A federal prosecutor then indicted Campbell on the following day…

- Gus Farber, a diamond and jewelry merchant from San Francisco, was prosecuted for the sale of thirteen $20 gold coins without a license. Farber, his father, and 12 others were arrested in four American cities after a sting operation conducted by the Secret Service for refusing to use the government’s new money…

- David Baraban had his business raided for possession of the “wrong” kind of money. David’s gold coins were seized and he was charged with conspiracy to defraud the United States…

- The Uebersee Finanz-Korporation, a Swiss banking company, had $1,250,000 in gold coins for business use. After transferring their gold to an American firm, they were shocked to find their gold had been confiscated. Instead, they were given paper dollars…

Money in America has been replaced before, by force…

Just as gold was turned into paper money at gunpoint… paper dollars will be turned into a central bank digital currency…

C-Day is already underway, and coming by September 19th…

How can I be so sure C-Day is coming and soon?

Because the U.S. government and the Federal Reserve are practically shouting their plans from the mountain top…

- On Jan. 20, 2022, the Federal Reserve announced a report detailing the next steps in launching a CBDC…

- On Jan. 21, 2022, Congresswoman Maxine Waters, Chairwoman of the House Financial Services Committee released a statement saying “…on central bank digital currencies, (the) report from the Federal Reserve is the first step in outlining the benefits and challenges with the United States’ potential issuance of its own CBDC…”

- On Feb. 3, 2022, The Federal Reserve Bank of Boston announced they were working with the Massachusetts Institute of Technology on a CBDC…

- On March 9, 2022, President Biden issued an executive order directing the Treasury Department and Federal Reserve to figure out next steps to launch a central bank digital currency…

And consider this:

Just weeks after Biden’s executive order, one of the nation’s biggest financial services providers announced it is building a CBDC prototype.

According to the managing director at this company, what they are building “…will maintain many of the existing elements of our currency today, so it’s effectively representing the U.S. dollar but in a digitalized form and on blockchain.”

In short, they are turning the U.S. dollar into a CBDC.

The pieces are all in place. The timeline is clear. There’s a Federal Reserve meeting scheduled for September 19th.

As a first step, I predict they will outlaw cash.

Then fully replace the dollar as we know it as a CBDC…

How to Protect Yourself on C-Day — And Position Yourself to Profit

I’m guessing the big question you have for me is… what are you supposed to do in the face of all this?

Well, I’ve spent the last 10 years researching solutions to this very problem.

The good news is I’ve discovered several simple steps you can take to protect your assets, and your way of life.

And not only this, but I’ve also found ways to potentially make a lot of money as C-Day unfolds.

Here’s what I recommend, starting at the most simple:

Your first priority should be protecting your own physical safety, and that of your family.

If you live in a city, I recommend you prepare yourself for riots, violent protests and food shortages. You should make plans to “bug out” if needed, and have a place to go in the countryside should cities become unsafe.

As I already showed you, things could get ugly very fast on C-Day…

Because most people are unaware of this threat, they respond with shock, and potentially violence.

The government will likely respond with price controls, rationing and travel restrictions… which will result in further shortages and chaos…

If you live in a rural area, you’ll have advantages of access to food supply from gardening and local farmers. I recommend you make the connections you need to ensure a supply of food and water, right now.

I also recommend you stockpile at least enough food and water to last at least 6 months. If you can afford more, consider making this investment in your physical wellbeing.

As far as protecting your wealth, to make sure you don’t lose everything and potentially even profit from this crisis?

Well, giving out financial advice like this happens to be my expertise…

That’s why I’ve put together a special package of other ideas to survive C-Day, and even thrive as the situation deteriorates…

Even if we only see inflation at 9-10%, these ideas should still position you to make a great deal of money in the coming years.

And worst case, you should still do very well compared to the overall market…

Plus you’ll have the peace of mind that comes with added security and privacy!

Keep in mind these are exactly the same sort of ideas I routinely provide high-net-worth clients and members of the U.S. intelligence community…

My speaking fee is over $25,000.

I’ve consulted with the Pentagon, the CIA, members of Congress, heads of state and even sitting U.S. Presidents.

But today, you can get my best ideas on how to prepare for C-Day for FREE, should you choose to take advantage.

Here are the specific steps I recommend taking today…

STEP #1: Use the “Nevada Secret” To Buying Gold For 6 Times More Profits

First off, I recommend you invest in physical gold and silver. Precious metals in the form of bullion and coins.

During past financial crisis situations, gold’s been a superstar.

In 1979, at the height of inflation of the Carter years, gold went up 136% in a single year…

After the 2008 financial crisis, gold went up as much as 185%…

I’m on the record forecasting gold could reach $15,000 an ounce in the next couple years.

After C-Day, all bets are off…

In the carnage which follows, my estimate for the potential of gold could be on the low-side.

In short: Get as much gold as you can afford. You’ll want at least 10% of your portfolio in gold.

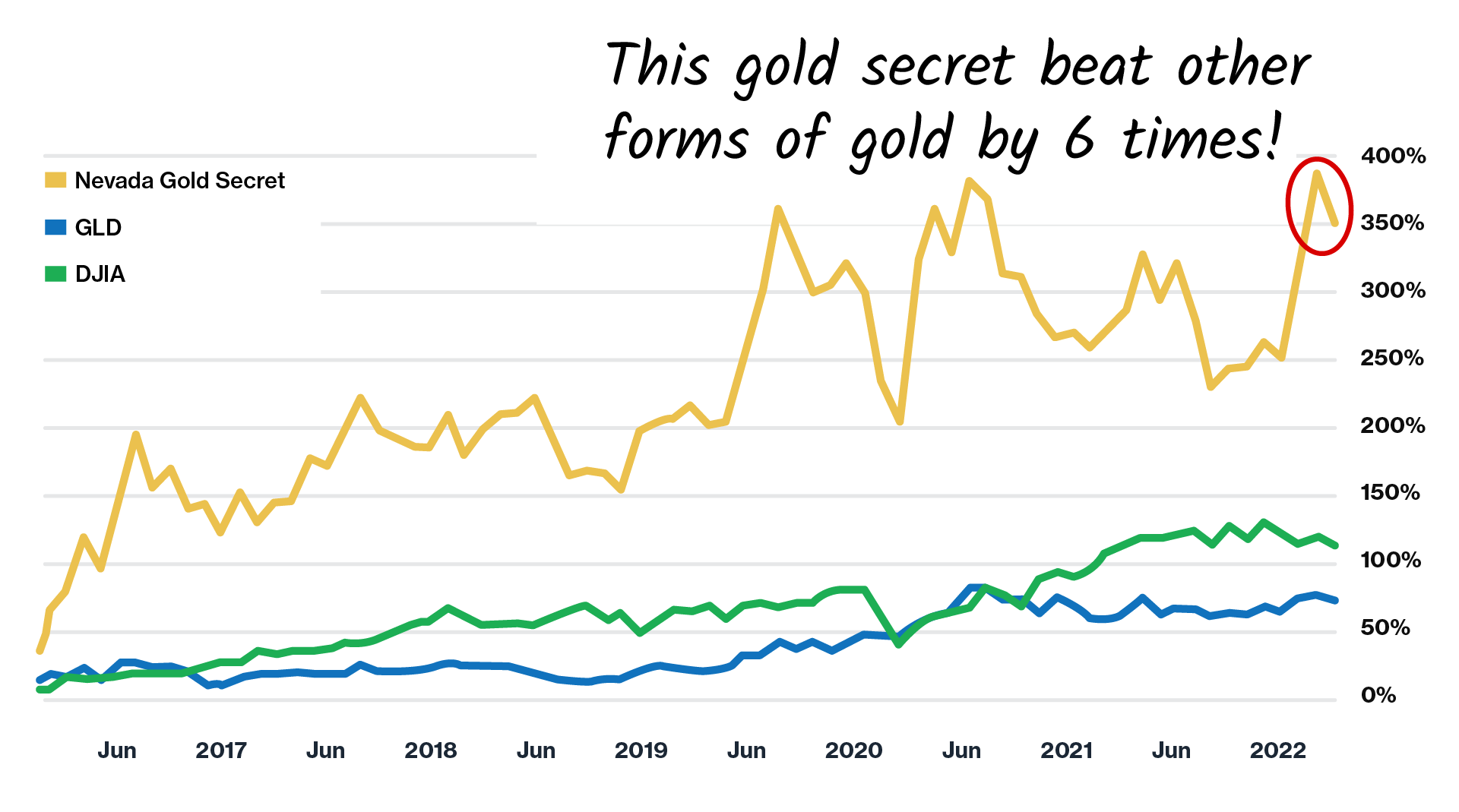

And not only that, you’ll want to learn my “Nevada Secret” for investing in gold for gains even better than other kinds of gold.

This secret has nothing to do with investing in gold coins, or anything like that.

I call it the “Nevada Secret” for the simple reason that this method of investing in gold was invented in the great state of Nevada.

And the best news, you can make 6 times more than what an investor would have made investing in other kinds of gold.

For example, there’s a security called GLD which trades on the stock exchange. It tracks the price of gold.

Well, over the past few years, this “Nevada Gold Secret” has beaten GLD by 600%…

That’s 6 times more than what investors in this other kind of gold took home!

Take a look at this chart:

Not only that, but the “Nevada Gold Secret” also did better than the overall stock market over the same period of years.

In fact, it gained 328% more than the Dow Jones Industrial Average.

I’ll show you exactly how this gold secret, and how you can take advantage of it immediately, starting today.

Everything you need to know is in my new report called: The “Nevada Secret” To Buying Gold For 6 Times More Profits.

I will gladly send you a copy right away, free of charge.

But that’s not all I want to send you…

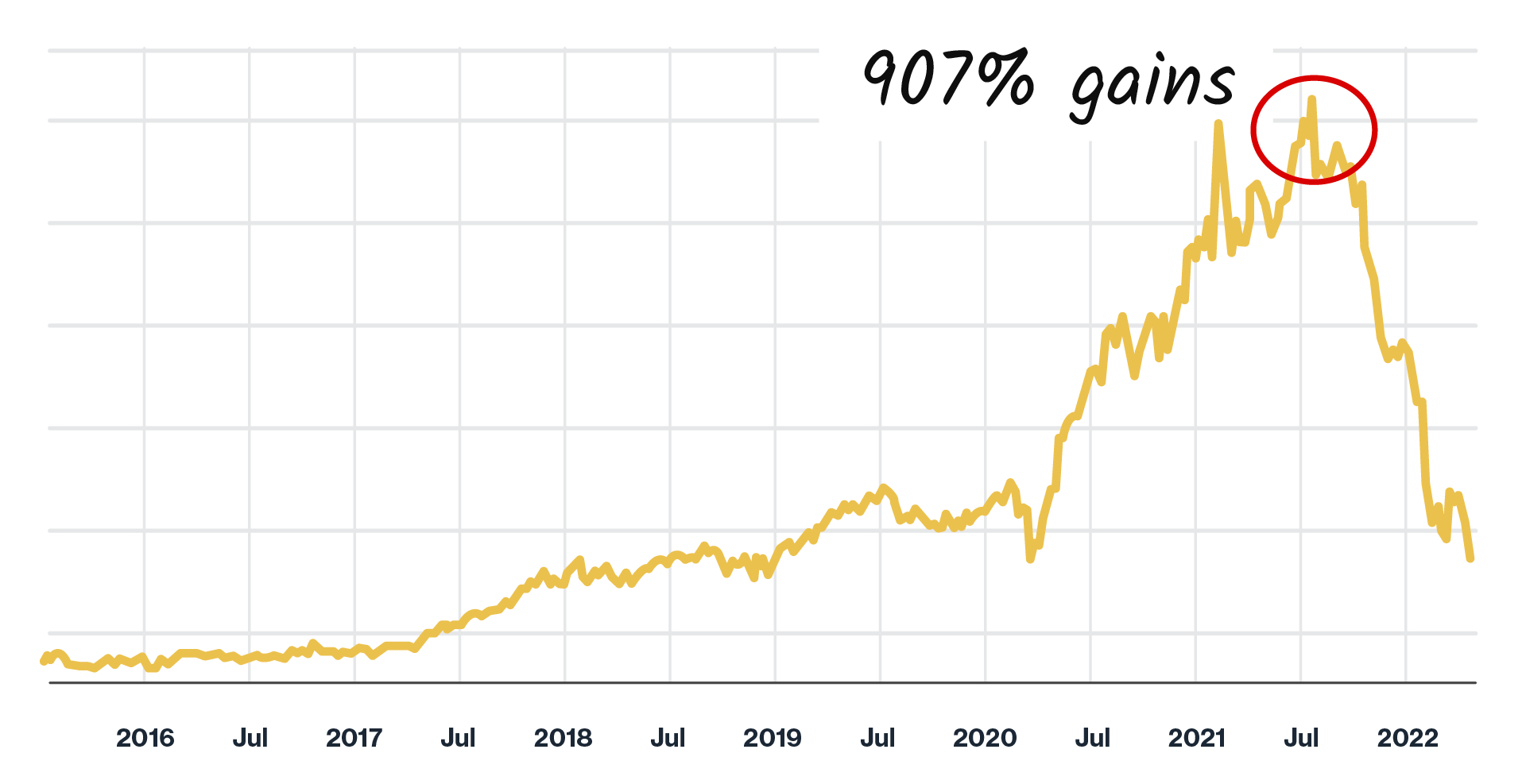

STEP 2: Grab the Chance for Huge Profits from the “C-Day Switchover”

As the central bankers turn “off” physical money flows around the world, someone will need to build the means to transfer and use the new digital currencies.

This switchover isn’t going to be cheap. The infrastructure isn’t all built yet.

There are 195 countries in the world — and huge parts of the world are still reliant on physical cash.

Many global corporations will be forced to pay through the nose to transact business.

This is already creating huge opportunities to make money…

If an investor had gotten into investing in the “C-Day Switchover” over the past few years, they would have enjoyed a 907% move to the upside …

That’s the same as getting 9 times money in return.

And the good news is profits from this “C-Day Switchover” should continue to grow…

Remember, one way to protect yourself from C-Day is to make as much money as you can.

This “switchover” is the perfect opportunity to do so. And that’s exactly why I want to send you another report for FREE today.

This report is called How to Ride “The C-Day Switchover” For Big Profits, and I’ll show you how you can instantly download it in minutes.

But hold on, because I want to show you something else…

Step 3: Learn How To Use The “2x Currency Trade” To Profit From Currency Wars

Over the past decade, nations around the world have used their central banks to devalue their currencies for geopolitical strategic advantage…

It’s played out exactly as I forecasted in my 2011 bestselling book, Currency Wars: The Making of the Next Global Crisis.

Can you guess what will happen after central banks launch fully digital currencies and replace paper money?

The answer is central bank digital currencies will be “nuclear weapons” in the next round of currency wars.

The next round of currency wars will cause even more financial chaos in the markets…

The effects of currency wars will ripple across the currency market — the stock market, and the options market.

You need to be ready. And more importantly, you can be in a position to even profit from these new digital currency wars.

How much profit? Enough to double someone’s money…

Potentially gaining 100% or more per trade, sometimes in only a matter of weeks.

To do so, you need to learn how to use what I call the “2x Currency Trade.”

This trading is not traditional currency trading. You don’t need to use the foreign exchange (Forex) market…

What I have for you is something new, and better…

I’ve been recommending the “2x Currency Trade” for years now, and many of my readers have had the opportunity to profit like crazy.

For example, back when Brexit happened, I recommended one of these trades, and it went on to gains of 150 to 200%…

In the recent past, I’ve recommended top “2x Currency Trades” for:

- 145% gains in 14 days on the Chinese Yuan

- 21% gains in 43 days on the Australian dollar

- 31% in 19 days on the South Korean won

- 37% in 24 days on the British Pound

- 68% in 17 days on the Brazilian real, and more…

What was my secret?

I’m happy to share with you, today.

You can get all the details on how to set up these kinds of trades in a special guide I want to send you, titled The “2X Currency Trade” Handbook.

The best news is you don’t need to know anything about currency trading to take advantage of the “2X Currency Trade.”

And with a little set-up (which I will show you), it’s possible to make these trades in your normal brokerage accounts.

You can grab The “2x Currency Trade” Handbook for free today, along with this…

Step 4: Make Sure You Have This “Off The Grid” Alternative Currency to Protect Your Wealth

With the death of paper money, you are going to want to have liquid assets to store your wealth, and to transact business “off-the-grid.”

That’s why I want to show you how to buy and use an obscure asset which works well as an alternative currency.

This asset is NOT a crypto-currency. It’s also not gold or silver coins.

I like this “off-the-grid” asset because it’s an inflation hedge, it’s portable and it’s worth more per ounce than gold.

This asset is practically untraceable. You don’t need to report possession of it to the U.S. government. You can easily carry it on your person, and also easily hide it from would-be looters.

If worse comes to worse, you can use this asset as a currency to trade with others…

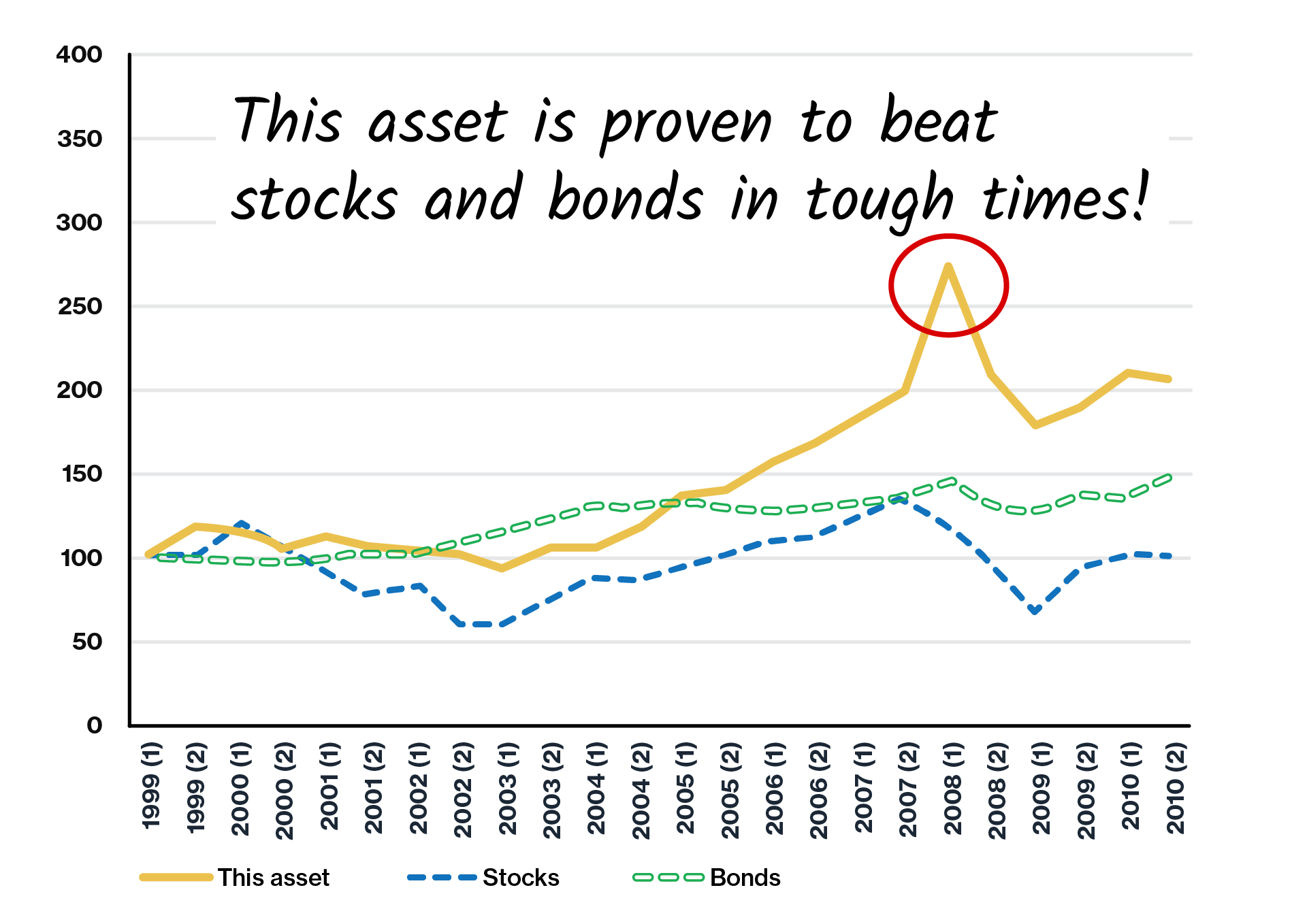

Legendary hedge fund Barton Biggs recommends this asset to protect your wealth.

According to Biggs, this asset was used by many to protect their wealth during and after the worst years of World War 2. Biggs says:

“When your neighbor’s children are starving (as so many were in the lawless winters of 1945 and 1946), they will do anything. If the barbarians come next time as a terrorist attack or a plague, you are going to want to have (this asset) close at hand…”

Best of all, this asset is proven to outperform the stock markets in tough times. In the rough years between 1999 and 2010, this asset outperformed stocks.

Today, this asset is performing well again. See for yourself…

I put everything you need to know about this asset in a special free report titled The Ultimate “Off The Grid” Currency.

You don’t want to wait. You will want to grab this report today. Here’s how…

What To Do Next…

I’ve worked hard to create a comprehensive plan to give you everything you need to survive and even thrive in C-Day.

Just keep in mind, I don’t have a crystal ball.

These strategies have given my readers amazing opportunities to profit in the past, but there’s no telling if they’ll keep performing the same way once C-Day hits.

But the way I see it, these reports are your best bet to protect yourself from the coming crisis.

To get your FREE access to these ideas, all I ask is you take a deeper look at my research.

All you need to do is take a test-drive of my flagship research newsletter service, Jim Rickards’ Strategic Intelligence.

You can try out everything I have for you today, at absolutely no risk or obligation.

In a few minutes time, if you accept this offer you can instantly download:

- REPORT #1: The “Nevada Secret” To Buying Gold For 6 Times More Profits

- REPORT #2: How to Ride “The C-Day Switchover” For Big Profits

- REPORT #3: The “2x Currency Trade” Handbook

- REPORT #4: The Ultimate “Off The Grid” Currency

Plus you get my monthly newsletter, Jim Rickards’ Strategic Intelligence.

My newsletter is where I will keep you up-to-date on all the happenings surrounding my C-Day thesis.

I’ll also be revealing some unique and unusual ways to make money from this situation, all explained as simply as possible, step-by-step.

But my service is MORE than a newsletter. It’s really a membership in a high-end service aimed at protecting your wealth and making you money.

The minute you join, you’ll get immediate access to all of the current membership benefits, including:

- You get a private access link that allows you to join an exclusive live intelligence session with me once a month.

This is where you’ll be able to get on a call with me and a small group of other members as I give you my analysis and update you on exactly what’s happening in the markets.

There will be a moderator and you’ll even be able to submit questions for me to answer.

Now remember I can’t give out any personalized investment advice, but this is as close as you’ll come to get your own personal briefing from the contacts I have in the intelligence community.

- You get invitations to all of our live events…

At these live events, you can hear from and shake hands with some of the biggest names in finance and investing.

People like Robert Kiyosaki, George Gilder, Ray Kurzweil, James Altucher, and more…

These events are typically hosted in high profile locations. Like the one we recently hosted in New York City.

And you’ll always be provided a special link that allows you to join online in case you can’t make it.

And all this is completely free for members of Strategic Intelligence.

- You get access to our private model portfolio updated in real time.

Here, you’ll get the chance to see dozens of opportunities my readers are already taking advantage of right now. These include investing ideas I didn’t have time to cover in this letter…

Now we get to your biggest question: How much does all this cost, and how can you get started today?

I’m going to make this super-easy. I’m not going to “hard sell” you on this.

I’ve put all my cards on the table in this letter.

And please remember, I’m NOT making this offer for the money.

In fact, my firm is likely going to lose money thanks to this special offer. That’s because it costs more money to advertise this offer than we will make back.

But that’s ok! This way I can prove myself to you — and build up a relationship for the chance for us to work closer together. It all works out for both of us in the end…

Normally, an annual subscription to Strategic Intelligence costs $99.

But today, I want to give you a trial subscription to my newsletter — plus all the special reports — plus all the other membership benefits…

All for a one-time fee of $49.

Remember, this is a trial subscription.

I’m taking all the risk here. If at any time during the first 6 months of service, if you don’t feel like you’re getting the best financial research available…

Simply call my team and we will give you a complete refund, no question asked.

You can even keep all of the reports and every issue I send you. It’s all yours…

Take all the time you need to decide.

But please remember that according to my latest research, “C-Day” could arrive as soon as September 19th…

It can’t be stopped. You simply must get ready. We still have time to get ahead of this thing, and grab profits…

Even if you don’t take advantage of my offer today, I hope you take whatever steps you can to prepare.

But I also believe with every fiber of being that my research and my investment ideas are the best solution you will find.

So don’t wait…

Simply hit the link below, and you’ll be directed to a secure order form.

Your order will be processed securely and instantly, and you can immediately download all my research in minutes.

RESERVE YOURTRIAL SUBSCRIPTION NOW

May 2023